For decades now, manufacturing companies have stretched thin their supply chains in the name of efficiency, says James Rickards in his latest book, Sold Out, in which he talks about broken supply chains, why the disruptions will linger for a while, and the path rebuilding supply chains from ground up to their new form – supply chain 2.0.

Rather than hunt for the cheapest materials or labour, manufacturers are starting to value the security that comes with shortening supply chains and building resilience, he states. “It will probably increase costs in some ways in the short run, maybe reduce margins to some extent, but is like buying insurance.” Since 2020, re-shoring has made a comeback and is part of the business strategies of manufacturing companies, that plan or have already moved production from Asia or China into the US or Europe. And, within Europe, Central and Eastern Europe (“CEE”) is highly ranked as a nearshoring and manufacturing hotspot. This trend is likely to accelerate further in years to come, explains Dirk Sosef, Head of Research and Strategy at CTP, continental Europe’s largest listed owner, developer and manager of logistics and industrial real estate by GLA.

Drivers supporting reshoring

“Due to all disruption caused by these (tragic) events, wellfunctioning supply chains and I&L real estate have become more important than ever before. “A higher safety stock of goods, de-coupling of global supply chains and rising online sales have resulted in an additional wave of I&L real estate demand. As disruptions are easing—for now—(reflected in, for instance, container freight rates) and the pandemic appears more under control, the effects are here to stay. “Companies are prioritising the more durable solution of de-coupling supply chains by re-shoring and nearshoring operations. In addition to risk mitigation, prioritising nearshoring is driven by accelerated wage growth in traditionally low-cost Asian manufacturing markets.” The trade-off between low-cost production in Asia and longer supply chains is no longer that attractive. The third driver supporting nearshoring demand is its reduced environmental impact: a company can significantly lower its carbon footprint by reducing the intercontinental transshipment of goods. The overall CEE region is expected to benefit most from this structural trend, as it offers a skilled workforce at competitive rates, strategic location adjacent to Western European consumer markets, and its improved infrastructure network,” Dirk Sosef points out for Automotive Tomorrow. CTP owns over 9.9 million sqm of space across 10 countries and is constantly growing its industrial and logistics parks in CEE to support its tenants’ growth. The company also became carbon neutral in operations in 2021, underlining its commitment to being a sustainable business.

Romania, Bulgaria, Serbia: Hotspots for business

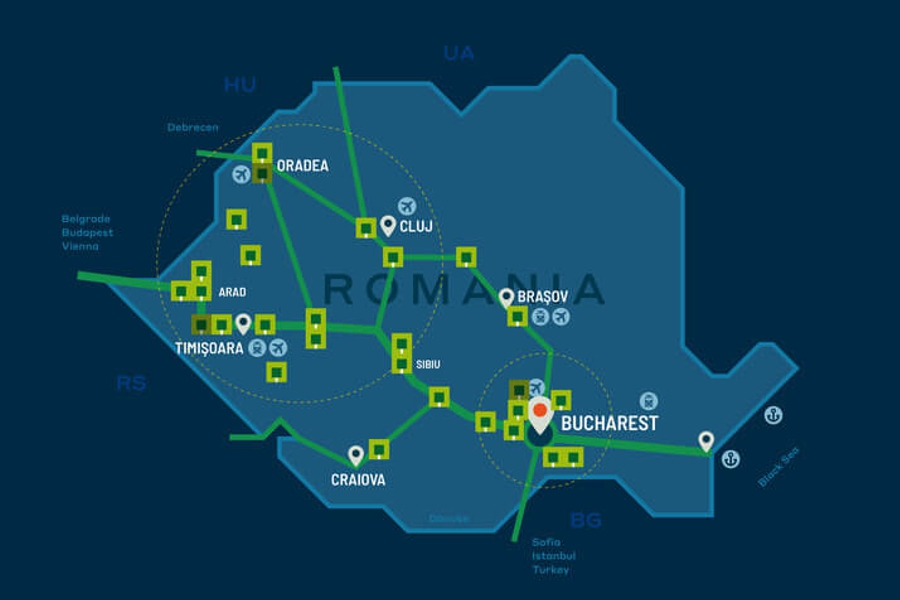

In countries such as Romania and Serbia, the company already has a strong footprint and is ranked as the market leader, while it is also building its presence in Bulgaria. “Emerging markets in Bucharest, Sofia and along the Hungarian/Romanian border, with ample land and labour as well as improving infrastructure networks, have the potential to develop into new regional or pan-European hotspots,” says Dirk Sosef. Demand is widespread, meaning not only capital cities, but on larger population centres. Main location decision drivers include accessibility of the workforce across all qualifications, proximity to suppliers and accessibility (road network). Markets outside the capital city have recently benefited from automotive/industrial manufacturing. Cities such as Oradea, Brașov, Timişoara, Pitești and Arad in Romania, Novi Sad, Kragujevac and Niš in Serbia and Plovdiv in Bulgaria are on the list of hotspots. Competitive labour rates for skilled and a motivated workforce, support from local and national governments and accessibility to neighbouring markets (including Turkey) and Western Europe are just some of the factors that attract investors. “An increased level of suppliers in proximity shortens delivery times and creates its own “eco-system” of new businesses, R&D institutions, and universities over time,” the Head of Research and Strategy at CTP concludes.

Dirk Sosef, Head of Research and Strategy, CTP “Many demand drivers (including nearshoring, re-shoring) in our industry are structural trends, meaning they are here to stay. The automotive and manufacturing industry has just started to build in higher resiliency by the de-coupling of supply chains and production, and therefore the CEE region is expected to see more demand in years to come. In addition, we remain fairly optimistic for this part of Europe, as it benefits from many other demand drivers as well (including undersupplied markets) and is increasingly important as a value-add production hub of Europe.”

{kind=link}